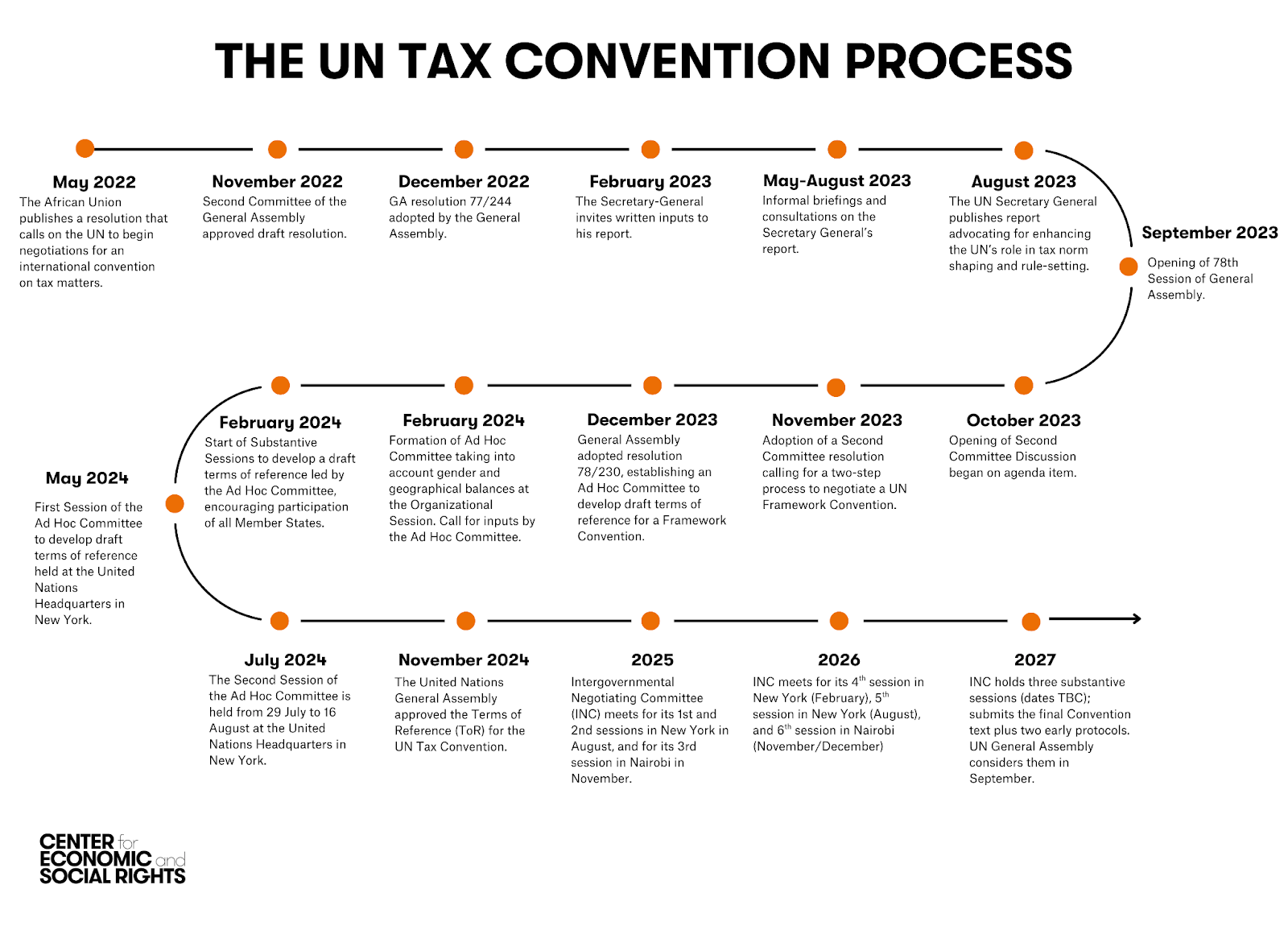

On February 13th, the Intergovernmental Negotiating Committee (INC) negotiating the future UN Framework Convention on International Tax Cooperation (UNTC) plus two early protocols (one on cross-border services, and one on dispute prevention and resolution) finalized its fourth substantive sessions in New York. As countries re-group online in inter-sessional (regrettably closed) meetings and prepare for the next in-person sessions in August, we discuss here some of the key issues that sparked controversy in February.

By María Emilia Mamberti, Research and Policy Lead, CESR

In recent weeks, we’ve been sharing daily updates from the sessions (see, for example, here) as well as a detailed analysis of the latest written submissions by States. As we discuss in said updates, debates on the Framework Convention have centered so far on the convention’s commitments. Briefly, some of the commitments that read less ambitious in the current draft (notably those on sustainable development and high net-worth individuals, the “super-rich”) showed more alignment among member States (called out for the need for more meaningful text by civil society). Instead, draft commitments on fair allocation of taxing rights -the very core of the Convention- and exchange of information evidenced tensions between many developing countries -most notably those from Africa- and some OECD members. Tensions often reflect opposing views on how transformative the UNTC should be, and its future impact on existing double taxation agreements and ongoing OECD work.

Now, as we await a revised draft of the Convention and the publication of a new round of written inputs, it’s worth looking at the broader picture. This blog therefore turns to some structural questions that remain unresolved for the UNTC. These overarching institutional issues sit at the very core of the negotiations and have surfaced repeatedly throughout the fourth session. Importantly, positions on these questions do not neatly follow the familiar North/South or OECD/non-OECD divides that shape many of the Convention’s substantive debates. Instead, they reveal something deeper: the profound political and institutional shift at stake in moving global tax cooperation discussions from the OECD to the United Nations.

The special features of taxation, and the relevance of earlier UN work

During the last INC sessions, some negotiators stated that taxation is a unique field and therefore rules emerging from the UNTC should be equally specific, with little to gain from looking at earlier processes in the United Nations to negotiate, approve and implement other framework conventions. This often came as a response to civil society proposals to build on learnings from other UN inter-governmental frameworks, and more specifically to demands for establishing a strong Conference of the Parties (COP) for the UNTC, akin to COPs from other treaties (we’ll get to COPs later).

Taxation is bound by specific principles (including simplicity, transparency, certainty and fairness) that would not apply to all areas of law equally, that much is true. Most importantly, core aspects of taxation are bound by the principle of legality (the virtually universal standard by which an act of taxation shall be based on a formal law, since “no taxation without representation…”). Some negotiators argue that legality is not so relevant to other policy areas, such as climate change, and therefore proposals for the UNTC that build from experiences in those areas are not truly relevant for the negotiations.

However, not all commitments that will fall under a tax cooperation treaty will necessarily equate to an act of taxation, implicate directly a decision on the sovereign power to tax, or entail a fiscal decision subject to the principle of legality. To the contrary, if we take the current draft text of the framework convention, we find provisions that States could discharge, arguably, without subsequent formal laws.

For instance, the current commitment on high net-worth individuals (HNWIs) or the “super-rich” includes a pledge to exchange information on the techniques used by these individuals (such as trusts and other and other opaque legal arrangements) to avoid and evade taxes. During the last sessions, States clarified that this provision did not refer to information on specific taxpayers, but to general information. Some (like Sweden and Mexico) further suggested exchanging information on best practices to target HNWIs, on top of challenges. The exchange of challenges and good practices in connection with a category of taxpayers, as a matter of tax cooperation, would not require formal laws. Such exchange is conceptually no different from the exchanges that happen within treaties from other fields, from which valuable insight can be gained. The same is true for the current text on capacity building and technical assistance -on which there was broad agreement-, which explicitly covers “administrative” (not only legislative) measures.

Furthermore, when States ratify treaties, they often agree to limit, to some extent, the sovereign decisions they can make through their national laws. For example, while current paragraph 9.b. of the UNTC’s terms of reference (ToRs) has been watered down from an earlier version that clearly stated extra-territorial obligations, the ToRs still commit to align tax cooperation with international human rights law. International human rights law contains, in UN treaties widely ratified by virtually all member States, a duty to abstain from sovereign conduct that would undermine other States’ ability to fulfil human rights.

We have also heard that existing work from other UN framework conventions or arrangements is not suitable to international taxation, as this is an intrinsically and particularly complex matter. However, complexity, fluidity, and uncertainty are pervasive characteristics of several public problems, such as addressing climate change, regulating AI, or dealing with pandemics. Indeed, one of the core reasons for using a “Framework-Protocol” approach to treaty-making is the need for flexibility in light of complexity. Literature specializing in governance of intricate problems has long identified the need for adequate regulatory frameworks under various approaches (such as adaptive management, democratic experimentalism, or anticipatory governance), noting the relevance of adaptability, ongoing monitoring and learning, and stakeholder engagement in these settings.

In the end, the negotiation of the UNTC is a ground-breaking process, in which all stakeholders bring relevant experience but also “learn as they do” on issues that are new to them. Practical learnings from existing UN work where other complex, fluid problems have been addressed with a whole of government approach (one ensuring collaboration and coherence among all relevant government agencies) are the safest way to proceed in this scenario.

The role of the future COP

The last sessions show that, while the existence of a future “Conference of the Parties” is a given for the UNTC, the actual scope and functions of the Tax COP are envisioned very differently among stakeholders. The International Law Commission defined a COP as “a meeting of parties to a treaty for the purpose of reviewing or implementing the treaty…”. While initially developed in the context of International Environmental Law, there are currently COPs pertaining to a wide range of subject matters covered by international treaties, from corruption and other criminal law matters to tobacco control. All parties to a treaty are represented in a COP (which often also engages other stakeholders), which meets regularly and functions as the “supreme body” of a convention. Two questions are open at the UNTC in this regard: first, what should a tax COP actually do; and second, what should the text of the UNTC say about its COP.

Some stakeholders -most notably, CSOs- argue for a strong COP, with concrete operationalizable mandates given throughout the Convention. Others argue that a tax COP cannot do much in the absence of formal laws, given the particularities of taxation discussed above.

Existing literature on COPs identifies and categorizes some of the key functions that COPs -well beyond the most widely known environmental COPs- normally perform, shedding light on what the future tax COP could do. Broadly speaking, COPs can both perform roles “within” and “outside” the formal operation of a treaty.

“Within” the functioning of a treaty, COPs can develop the content of the agreement, set procedural and substantive standards, adopt their internal procedures, deploy reporting systems and other arrangements to monitor compliance, make recommendations, perform interpretative functions, resolve disputes, establish subsidiary bodies, and, broadly speaking, develop norms. Therefore, COPs conduct both actions that are internal to the operation of a treaty, and others with direct effects on the parties’ obligations.

COPs conduct normative activities because they produce acts to instruct the behavior of the parties on how to comply with treaty commitments. COPs can use different tools for this end, including some that call for further national-level ratification (such as adopting protocols) and some that don’t (such as issuing guidance). The use of guidance, commentary and other forms of interpretative, soft-law instruments is pervasive when addressing complex issues, including international tax (as the prolific soft-law work of the OECD on the matter, routinely observed by many Member States, illustrates). Of course, the intensity of norm-setting work can differ from COP to COP. Literature has found, for example, that COPs of treaties that relate more closely to sovereign issues (such as criminal laws) may produce comparatively less normative outputs than other COPs.

Importantly, COPs also have impacts “outside” the functioning of a treaty, through incentivizing national-level measures (for instance, by “building momentum for the implementation of the treaty”, or “stigmatizing adversaries to the treaty”). Recent academic work has documented extensively, for example, how the Paris Agreement played a catalyzing role for climate litigation, creating new opportunities at the national level for social and legal mobilization. Some of the commitments contained in the UNTC are particularly well suited to trigger independent national-level reform, such as the pledge to tax HNWIs effectively (as the recent experience of France discussing a “Zucman tax” after the issue made it to the G20 agenda shows). Arguably, the commitment on sustainable development, if sufficiently well-designed, could similarly open the door for national level reforms supported by active work of the tax COP.

Finally, during the last sessions some argued that the tax COP did not need specific mandates in the UNTC, as COPs have implicit authority by their own “nature”. Yet, with other CSOs, we stress the need to distill some functions of the COP and provide it with both broad and concrete mandates within the Convention itself, to steer its future work. Indeed, many conventions do set precise mandates for their COPs, and for good reason, without prejudice to the “implied powers” COPs can normally exercise.

Other structural issues to address in the next sessions, and what to expect next

At least two other "overarching" issues remain open, which have the potential to diminish the ambition of the whole process. First, how countries interpret the bindingness of a framework convention. Unfortunately, some countries -probably most notably Canada- appear to conflate a framework convention with a mere political framework. However, countries cannot commit to not commit within a legally binding treaty.

Legal mandates can grant their recipients significant discretion for implementation. This is normally the case under international law, where countries have the capacity to choose implementation measures that better respond to their national realities. Furthermore, international law commitments do not always require immediate outcomes from bounded countries. As we discuss elsewhere, commitments may only carry obligations of conduct or means (to “try one's best” or make a deliberate endeavor), but not to achieve specific results or outcomes. Obligations can also be positive or negative, and of immediate or progressive realization (recognizing that certain outcomes take time). Yet they are still binding obligations. Furthermore, including the term "framework" in the name of a treaty has no legal consequences. Briefly, a framework convention is a treaty of international law that is binding like any other treaty. The particularity is that it establishes broad and general, instead of fully-fleshed, commitments, which are later elaborated in additional tools (such as national-level or COPs decisions, additional protocols, etc.). In other words, high-level/not detailed does not equate to non-binding/voluntary.

Second, the relationship of the UNTC to other agreements (to be defined in current article 15 of the Convention’s draft) triggered deep divisions between North and South countries, given the North general resistance to accepting the UNTC could either supersede existing double taxation agreements, or the work of the OECD. Yet there are no legal reasons why a future treaty with the same subject matter and parties could not override an existing treaty, especially if needed to achieve the object and purpose of the UNTC: to establish fully inclusive and effective international tax cooperation.

These issues are likely to come up again during the August sessions, and we’ll be reporting back on these and related topics. More specifically, we expect that a draft article on the “Relation with Other Agreements, Instruments and Domestic Law” (article 15) will be released in advance to the August session. Stay tuned for more updates!